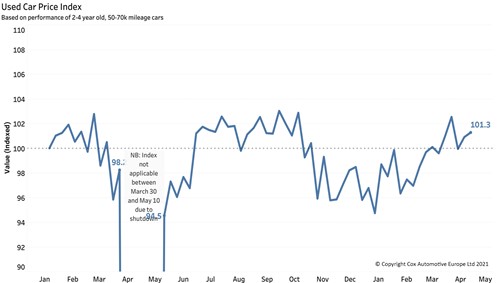

Positive auction performance highlights dealers’ return

The reopening of physical showrooms across the UK in the early parts of April has resulted in positive auction performance in the first half of the month. While comparisons to 2020 are impossible due to the first lockdown, average wholesale car prices for the first 16 days of April 2021 are at £6,448, a massive +£846 (+15.1%) increase compared to the same period in 2019.

Compared to 2019, CAP Clean performance (+4%) and first-time conversions (+2%) are also up, indicating that buyers are returning to auctions to replenish stock sold since the reopening of their dealerships.

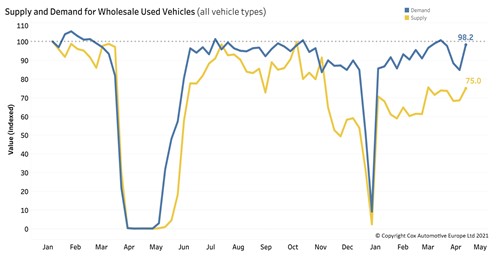

Used car supply problems continue, but demand increases

Used car supply has steadily increased since the start of 2021, however volumes remain below what we’d expect to see at this time of year, and crucially down compared to the period last summer between the first and second lockdowns. As we reported in AutoFocus, we anticipate used car supply constraints to continue throughout the first part of the year, but optimistically we are expecting a release of newer and lower mileage fleet stock into the market.

Demand continues to improve in April, supporting the market sentiment that the reopening of physical showrooms has created a requirement for fresh stock. However, a perfect storm of low supply and high demand could see prices continue to increase in the short-term.

New car market bounce back expected in Q2

New car registrations at the end of March 2021 are -12% (425,525) down year-to-date, however, with the reopening of physical showrooms at the start of April, a modest bounce back is expected in the new car market. The release of pent-up demand from the recent lockdown will see sales recover but this is unlikely to be to the same levels we saw on the back of the first lockdown.

Although new car targets for dealers are reported as realistic and consider the current restrictions, retailers are fearful that manufacturers will adjust targets upwards on the back of a good Q2.

As we reported in AutoFocus, Cox Automotive has forecast a most likely scenario of 520,835 new car registrations for Q2 this year, representing a -5.9% drop compared to the 2000-2019 pre-pandemic average. This scenario assumes some modest pent-up demand in April and May, but with remaining consumer nervousness holding back a full recovery.